Summary

Last year, we released a three-report series that outlined a couple methods to predict recessions and monetary policy pivots. Today, all three major tools still signal a recession within the next year. Despite the odds of a soft landing rising amid resilient economic data, the framework aligns with our base case expectation for a mild recession in early 2024.

Three’s a Trend

Last year, we released a three-report series entitled Is Recession Coming? that outlined a couple methods to predict recessions and monetary policy pivots. The economic landscape has shifted since we published that series—the fundamental components of the economy have performed better than anticipated in recent months despite the aggressive pace of policy tightening from the Federal Reserve. Economists are growing broadly divided on the prospects of a near-term recession, so we take this opportunity to update and revisit the series’ major tools.

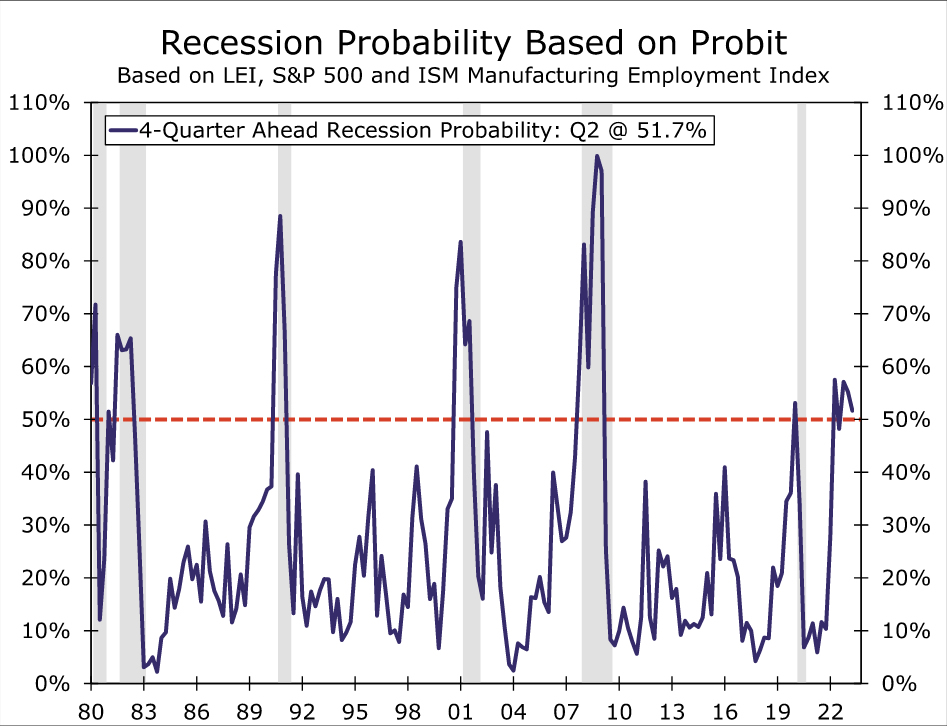

The first tool is our preferred Probit method, which is based on the Leading Economic Index, the S&P 500 and the employment component of the ISM manufacturing index. The method estimates that the probability of a recession fell to 52% in Q2, down from 55% in Q1 (Figure 1). While the probability has slipped, it has been above 50% in four of the past five quarters. Historically, when this Probit’s probability has surpassed 50%, the economy experienced a recession within the next four quarters. In short, our Probit framework suggests that recession within the next year is still more likely than not.

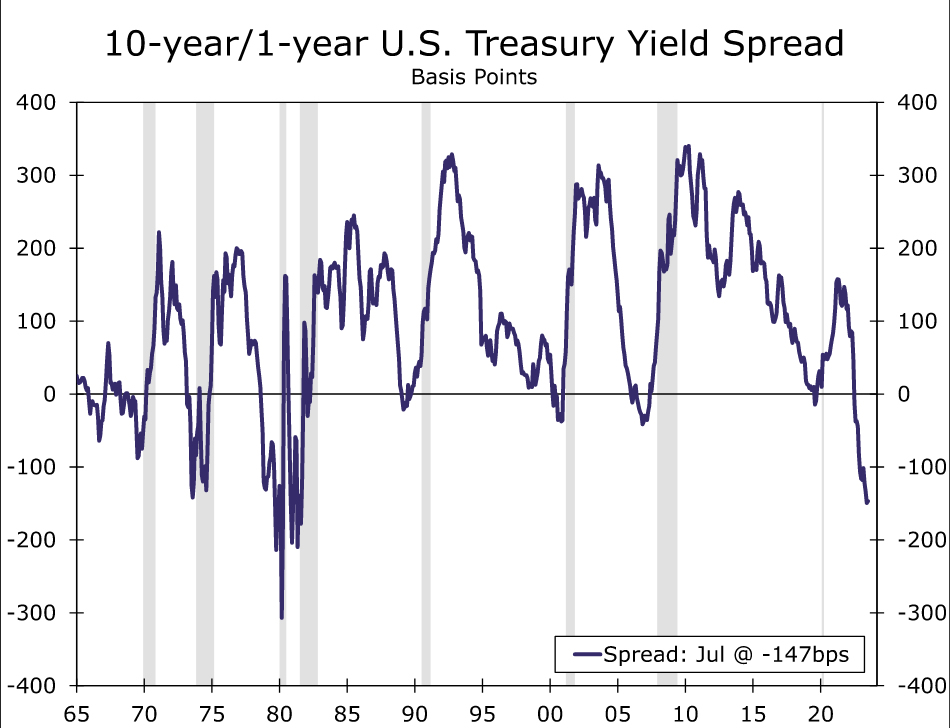

The second tool is the spread on the 10-year and 1-year Treasury yields. Using a recession-prediction threshold of two consecutive months of inversion, the yield spread has predicted all the past 10 recessions, with an average lead time of 12 months. Through July, the spread has been negative for 13 straight months (Figure 2), signaling a recession is indeed on the horizon.

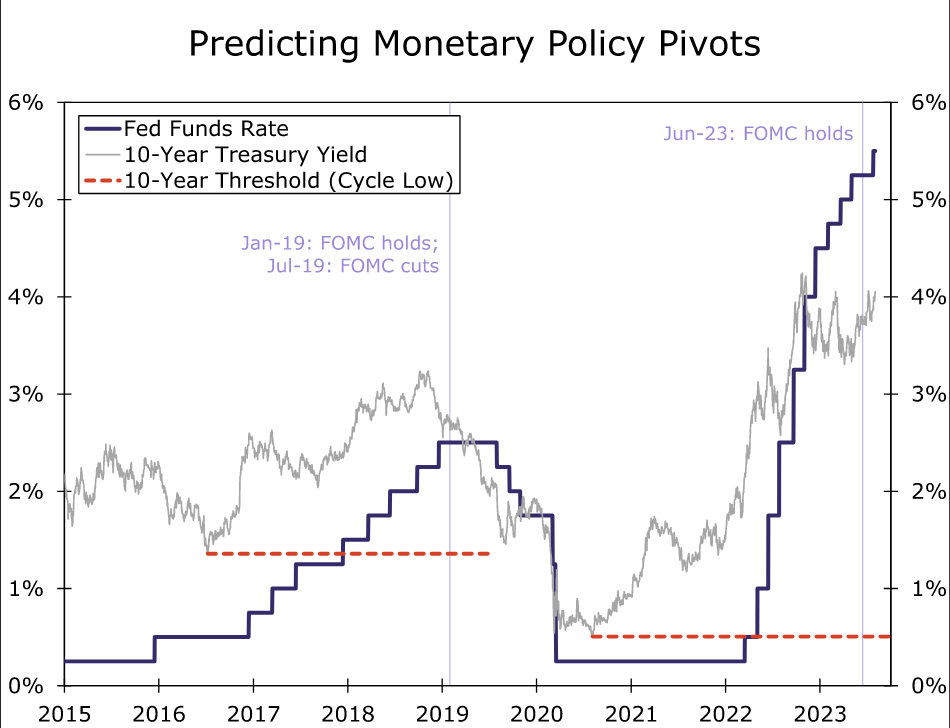

The final tool is a threshold method that uses the 10-year Treasury yield and the federal funds rate (FFR). In a rising interest rate environment, we found that when the FFR crosses the lowest 10-year yield in that cycle (the threshold), a monetary policy pivot is likely to ensue in the next 18 months. As shown in Figure 3, the FFR crossed the 10-year’s current cycle low back in March 2022, when the FOMC kicked off its tightening cycle. The FOMC decided to hold rates steady in June, 16 months following the threshold breach. While the FOMC elected to hike the FFR by 25 bps to a target range of 5.25%-5.50% in July, the threshold approach suggests a pivot to an accommodative stance is in the offing, which historically occurs amid slowing economic growth.

In sum, all three tools signal a recession within the next year. Despite the odds of a soft landing rising amid resilient economic data, the framework aligns with our base case expectation for a mild recession in early 2024.